The Seat Cost vs Trip Cost Paradox

Oversaturation in the large narrowbody market showcases the profitable use cases for the smaller aircraft.

Author: Courtney Miller – courtney@visualapproach.io

Commercial aviation is a growth industry. Despite the occasional economic, geopolitical, or viral speed bump, air travel continues to grow alongside global economies. Yet even though this growth in air travel continues alongside its economic engine, it arrives in different forms.

A key driver of this growth during the past two decades has been the demand for ever-lower-cost service. Reducing the cost of travel has worked to provide access to entire communities for whom it was once far too expensive. The focus for airlines was on reducing the total cost per seat, which enabled the low fares that drove so much of the growth.

Yet the same drive that propelled airlines to deliver the lowest cost per seat eventually drove the purchase of increasingly larger aircraft. Airlines that once relied on a low-cost sweet-spot near 100 seats have since grown average aircraft sizes in search of lower seat costs to today’s most popular low-cost capacity – 240 seats. This 240% increase in seat gauge brought the lower seat costs desired, but at an ever-dwindling number of markets for which an aircraft that large could be deployed.

And so growth has slowed. Airlines focused on deploying larger aircraft to achieve the lowest cost per seat, risking empty seats as the number of markets supporting 240 seats is quickly consumed. Once consistently profitable, ultra-low-cost airlines are now dealing with market saturation from prior years of growth while being limited to the largest aircraft available to sustain that much-needed growth.

This analysis challenges the assumptions that the ultra-low-cost model is exclusively dependent upon the large narrowbody. We look beyond the focus on seat costs alone as the driver for growth, to the untapped opportunity in the seat gauges that originally built the low-cost air travel sector. We consider the balance between seat costs and trip costs and quantify untapped growth potential for a cohort of aircraft built for the origins of low-cost growth – the small narrowbody.

The seat cost growth trap

The endeavor to lower the total cost per seat is virtuous. Lower seat costs allow for lower fares, which in turn, encourage more passengers to fill them. Their ability to drive growth is proven and powerful as entire populations enter the middle class.

It is the method by which airlines achieve low seat costs that can work against growth opportunities faster than they enable them. For instance, there are two ways to lower the cost per seat on a flight: reduce the costs or increase the number of seats.

As is evident in almost any business, reducing costs is difficult. Labor costs steadily rise, aircraft ownership costs continue to increase, and fuel costs are largely out of airlines’ control. While not impossible, overall costs can only be managed within a certain bandwidth, for which low-cost airlines are obsessed.

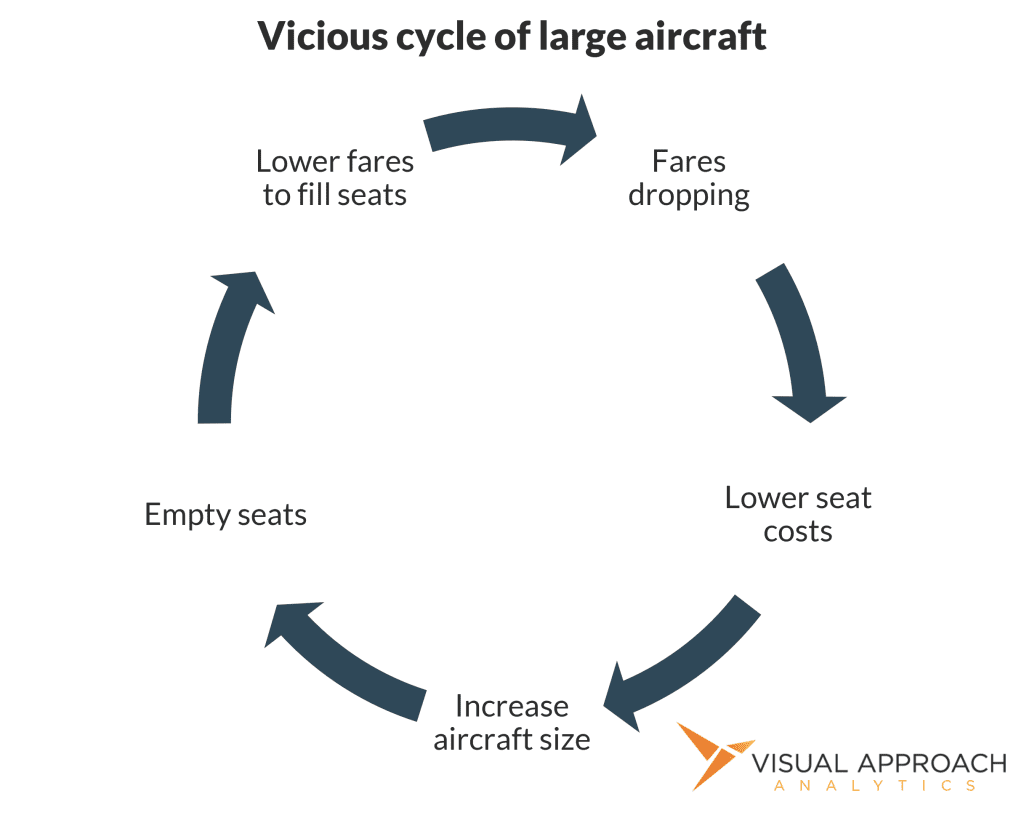

While lowering costs has been a continual fight in the drive to deliver low seat costs, the ability to add seats has been a much more effective method. Lowering overall costs by 10% can be a major undertaking, but increasing the size of an aircraft to the next gauge can deliver a 15%-20% reduction in seat costs almost immediately. This narrow focus on seat costs (supported by very enthusiastic aircraft manufacturers) has created an incentive to increase aircraft capacity at almost any cost and is the driver behind the industry’s evolution from 100-seat to 240-seat aircraft.

Following the above graph’s vicious cycle of large aircraft from the right, the attempt to lower seat costs drives the need to increase aircraft size. As a result, many more seats must be filled, resulting in fares being lowered to attract those incremental customers. While those low fares were offered as the solution to empty seats, they quickly became the problem. To maintain profitability at low fares, seat costs must be reduced, for which we’ve already deduced that the best answer is to increase aircraft size… The cycle continues.

Over the past 40 years, this cycle has been sufficient. Low-cost airlines have been able to grow into new regions, keeping seat costs low by increasing aircraft size, while the seemingly insatiable low-cost traveler continued to arrive in increasing numbers. The model works – until it doesn’t.

Even though growth has been consistent and seemingly originating from a bottomless source of demand, markets eventually become saturated. Much of the growth in prior decades has been from new markets without low-cost service, a powerful driver that could fill aircraft despite their larger size.

Markets cannot grow indefinitely, however. An unillustrated downside to seat-gauge growth is that each time aircraft sizes are increased, the number of markets large enough to support them decreases. This matters little when sufficient growth can be found elsewhere, but the low-cost model is no longer new, and many of the markets that can sustain aircraft with 240 seats have already been found.

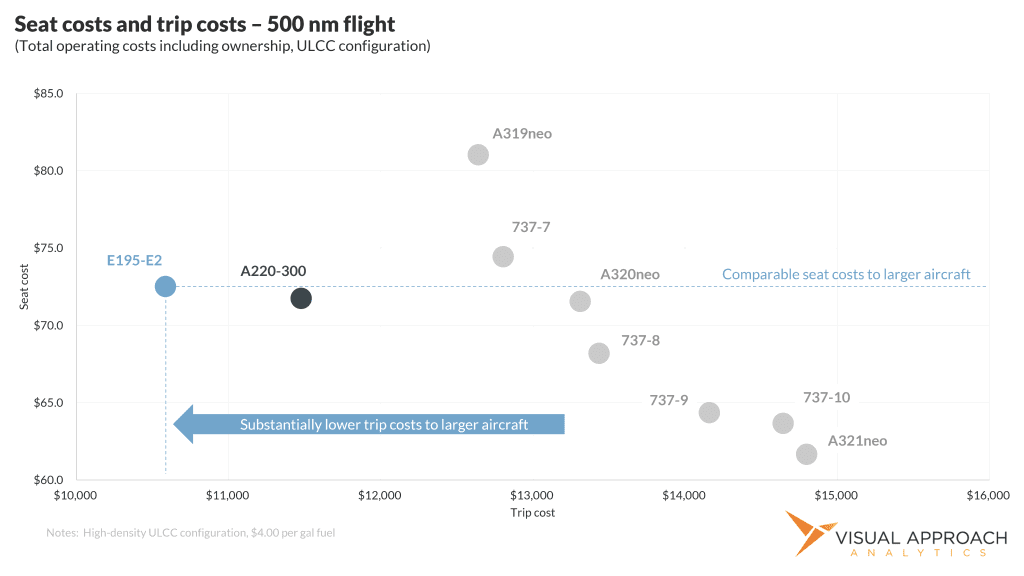

While the large narrowbody truly does deliver the lowest seat costs in the market, it also offers the highest trip costs. With higher trip costs comes a reduced number of markets that can support this cost. As the large narrowbody continues to grow into dwindling markets with low seat costs but high trip costs, a new balance is available to create economical access to new markets, furthering the growth once enjoyed by the industry. Today, the candidate best positioned to find this balance between profitability and growth is the small narrowbody, e.g., A220/E195-E2.

Finding the trip-cost/seat-cost balance

The narrowbody market today is dominated by the Boeing 737 and Airbus A320 families. Focused around a common design for each family, the lowest seat costs can be found at the largest aircraft in each family. For the 737 family, the lowest seat costs will be with the 737-10, and the A321neo currently delivers the lowest seat costs for the A320 family.

In similar fashion, the small narrowbody families of the Airbus A220 and Embraer E2 see the lowest seat costs at their largest variants. For the A220, this is the A220-300, while the E195-E2 delivers the lowest seat costs for Embraer’s family. This optimal balance between trip and seat costs rests at the largest member of each family, yet by considering aircraft across aircraft families, a new balance can be found.

While the A319 and 737-7 do not deliver sufficient trip cost reductions for the loss of seats compared to the A321 and 737-10, the A220-300 and E195-E2 do. For an airline to consider a 156-seat A319neo compared to a 240-seat A321neo, the smaller A319 would deliver 15% lower trip costs, but with a 31% higher seat costs. Certainly, the lower trip costs could open new markets, but the sharply higher seat costs present an imbalance to the airline. It’s better to continue with the large narrowbody. The dynamics that have driven the low-cost market to the largest aircraft make sense.

The new aircraft families offered through the A220 and E2 shift this dynamic. A 146-seat E195-E2 would certainly increase seat costs compared to an A321neo – 16% in this example.

However, the E195-E2 would also reduce overall trip costs more substantially. The 16% increase in seat costs would be accompanied by a 39% decrease in trip costs. The traditional view is that it would not be worth considering smaller aircraft because the benefit in trip costs is swamped by higher seat costs. Today, that dynamic is inverted with the arrival of the new small narrowbodies. This opens new opportunities for airlines to reconsider paths to growth beyond simply acquiring the larger airplane.

From seat cost fixation to profit specialists

The step change in the balance between seat and trip costs is one the industry has not seen in over three decades. Multiple careers have been built with the knowledge that it is not worth the increase in seat costs to shift to a smaller aircraft.

Suddenly, though, that 30-year “truth” has been upset. It is no longer sufficient to simply assume that solving for seat costs alone will deliver the greatest earnings potential for an airline. Rather than driving for larger aircraft with lower seat costs, the growth opportunities opened by the new small narrowbodies require a different assessment of the market.

This new balance brought by small narrowbodies drives new ranges for which larger narrowbodies are best utilized. Considering $100 in revenues per passenger (fare and ancillary fees included), a small narrowbody will start delivering profit in markets with only 90 passengers. This low break-even load factor is not uncommon, as the A321neo with 240 seats would break-even at only 129 passengers at this fare.

Yet, even as passenger demand increased along certain routes, the small narrowbody would remain more profitable than the large narrowbody until it filled every seat. Yet, what is often overlooked is that the small narrowbody would remain more profitable in larger markets up to 190 passengers, effectively turning away passengers for more profit than accepting them on the more expensive large narrowbody.

And yet, in markets where 190 passengers are willing to pay $100, the large narrowbody remains the most profitable option. The result are two clear profit zones. Where the A321neo required 129 passengers all the time to break even, the small narrowbody can do so with 30% fewer passengers. Yet, where the markets have higher demand, the large narrowbodies fill seats and beneficial seat costs deliver higher returns.

In this way, the small narrowbody is not a replacement for the large narrowbody, rather a supplement to unlock new growth while allowing the large narrowbody to focus on the most profitable routes.

Unlocking incremental low-cost growth

The large narrowbody works incredibly well in the low-cost airline business model. Indeed, the industry-leading seat costs presented in this analysis confirms just that advantage.

However, it is the limitation of growth opportunities that the largest of the narrowbodies presents alongside the seat cost advantages that ultimately catch up to growing low-cost airlines. Eventually, large airplanes run out of markets.

To be certain, small narrowbodies would also run out of markets. However, the lack of substantial deployment of small narrowbodies within the low-cost segment today leaves significant untapped potential. This potential can also be quantified, particularly in a large market such as the United States.

The low-cost airlines in the U.S. have been in growth mode for the past two decades. While Allegiant continues to effectively deploy its small market strategy, Spirit and Frontier have followed the ultra-low-cost recipe to a “T”. Both starting with A319 aircraft, the two airlines have grown to an orderbook primarily comprised of high-density A321neo aircraft.

The two airlines also grew from different areas of strength across the country. By early 2015, Spirit dominated South Florida, the East Coast, and the Caribbean, while Frontier dominated Denver and the West. The two airlines continued to grow, and eventually grew into each other, colliding as the number of available unserved markets dwindled.

By 2026, data shows that approximately 127 viable non-stop markets remain in the United States that could support new or increased A321neo service. However, most of these markets already have nonstop service, even if the total number of seats lags total demand. Further, many of the markets without nonstop service are those that cannot be operated due to other restrictions, such as range, airfield limitations, or other regulations. For example, a top underserved market is New York Laguardia (LGA) to Los Angeles (LAX), yet this route can only be served nonstop on Saturdays due to the 1,500-mile perimeter rule.

Further complicating matters for large narrowbody new market growth is the reality that if a market is large enough to be viable for a 240-seat A321neo, other low-cost competitors know about it and are almost certainly already in position.

Conversely, a small narrowbody could open more routes to new market growth for an expanding low-cost airline. In our simple example of the U.S. domestic market, 264 markets stand out as growth markets for the small narrowbody, many of which have no competition at all.

Further, the addition of the small narrowbody into growth markets further weakens growth for the large narrowbody as many of the routes viable on the large narrowbody are more profitable using a small narrowbody. The result is 264 new market opportunities where the small narrowbody remains the most efficient option, compared to the 53 for the large narrowbody.

Indeed, this outlines much of the strategy for rapidly growing Breeze Airways, which has been successful at opening new low-cost markets with the A220-300 small narrowbody. While Spirit and Frontier are looking to return large narrowbodies, Breeze continues to grow into the plentiful number of new markets made available by the A220.

Ultimately, it is this drastic shift in reconsidering what drives the success of the low-cost airline business model that is already driving airlines back to the small narrowbody. The large narrowbody has built the backbone of the low-cost airline community, and will stay the flagship for years to come. Yet, for all its virtues, the growth will come from the airlines willing to reconsider the rules of yesteryear and find a new growth balance with the small narrowbody.

Falko is a leading aircraft lessor and asset manager focused on the 70 – 130 seat aircraft segment and is one of the longest standing lessors and managers of aircraft of this size globally.

If you are interested in learning more about investing in small commercial aircraft, please contact Falko’s Investor Relations team at Investor.Relations@falko.com.